The Only Game in Town: The Stock Market

The Stock Market is an enigma to many people. It’s never discussed exactly how it works, what the S&P Index actually means and if/how it impacts our everyday lives. One thing seems for certain though: it is (likely) the only game in town for the everyday investor.

Putting aside crypto and newly founded prediction markets, the US stock market is the most accessible investment vehicle for most people. There are other ventures that investors can pursue; Real Estate, Private Markets, Commodities such as Gold, entrepreneurship and even just saving money. Most of these, however, are either reserved for ‘Accredited Investors’, meaning you make a certain income and have a certain net worth, or too cumbersome for someone with a full-time job to commit to.

The Stock Market is simple enough for most people to start with and has a low barrier to entry: you open a brokerage account, fund it, and begin trading. Most people will buy an Exchange Traded Fund (ETF), meaning a fund that invests in many stocks or other assets, and just keep the investment. Investors also have the option to buy ‘fractional shares’ of companies and ETFs if they do not have enough funds for a full share, meaning any amount of money can be invested. Workers who have retirement accounts through their employment via a 401(k) or 403(b) are usually invested in the stock market, whether they realize it or not.

This does contrast from the American Dream many were told about: full time employment, a family comfortably supported and, most importantly, home ownership. Many consider their home their largest investment (which I disagree it’s an ‘investment’, but that’s for another day).

Home ownership in 2026 America has become unaffordable for most. An estimated 43% of working Americans can afford the average home, compared to 65% home ownership participation. This shows that many are priced out of the housing market, and even some that made their way in are potentially financing their lives with other debt to keep head above water. By contrast, stock market participation is at all time highs at approximately 62% (up from just 10% in the early 1970s), as many Americans are deciding to put more money in their retirement accounts and open taxable brokerage accounts instead of pursuing home ownership.

Why is this? The answer: 1971.

This is the year the United States government, with President Richard Nixon in office, detached the US Dollar from Gold, ushering in the era of modern ‘Fiat Currency’. This meant that there was no longer a fixed exchange rate between the dollar and gold, the two could trade freely, and the dollar was no longer backed by gold. Instead, the dollar was now backed by ‘The Full Faith and Credit of the United States Government’. This allowed the government to control money supply as they saw fit, which generally meant printing more money, leading to inflation.

Simple economics: the more there is of something, the less valuable it is.

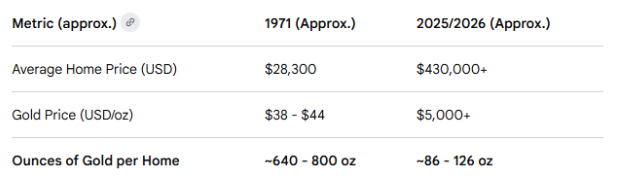

Every year, a person’s savings loses 2-3% (sometimes more) of its value due to inflation. Over a 55 year period this compounds greatly against a person. Since the dollar continues to lose value, the assets or securities you can buy with it have to go up by definition. Home prices have increased greatly since 1971: the average home price in the United States is now $430,000 vs $28,300 in 1971, a cumulative increase of about 15 times. By contrast, the real wage growth rate of workers, so adjusted for inflation, is just 15 percent! This means the dollar has lost roughly 87% of its purchasing power in this timeframe.

So has housing actually become more expensive, or is it just a currency devaluation? To answer this, we’ll need to compare home prices over this time period to other assets, particularly assets that everyday investors could theoretically participate in. This would be Gold, and the Stock Market as measured by the S&P 500.

Over this timeframe, the average home price has decreased significantly in terms of Gold and the S&P since these assets have appreciated in value. The table below shows the average home price in 1971 and today in gold:

Housing prices in terms of Gold have decreased approximately 85% since 1971.

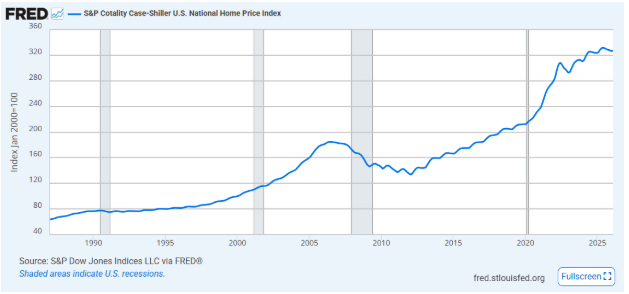

Similar to gold, the S&P 500 has also far outpaced housing prices, meaning that housing prices in terms of S&P shares have dropped significantly as well:

What does this tell us? First and foremost, people need to invest since holding only cash is risky. People should keep some money in savings in case of emergencies, generally 3-6 months of living expenses is advised. These savings should also be in an interest-yielding account, ideally around 2-3% so it is offsetting the inflation cost. Beyond that, it is inefficient to hold excessive amounts of dollars.

Second, the Stock Market is the most reasonable avenue to investing for most everyday people.

Couldn’t people invest in Gold, however? Sure they can, but buying physical gold is cumbersome. One would need to go to a certified dealer and verify the gold is real, pay for it (usually over the spot price to compensate the dealer), then pay storage fees to hold it, unless one is willing to take the risk of having it in their home. To sell it, a similar process would need to occur, which will take time.

To invest in gold, many folks turn to the securities markets and buy an ETF that tracks the price of gold or companies whose value is tied to gold, such as gold miners. Stocks and ETFs generally pay a dividend to investors, unlike gold, giving the investor some cash flow while they hold the security. Therefore, the Stock Market is the only feasible option for the everyday person of average wealth to invest these days. This is a large reason why the stock market continues to generate superior returns to almost any other asset class and remain at, or close to, all-time highs.

While market corrections and crashes are inevitable, it is generally advised to stay invested through these market turbulences. Since our assessed timeframe of 1971-2026, there have been several crashes and corrections of stocks, yet the long term returns are hard to argue with.

The continuous devaluation of the US Dollar (and every fiat currency) has caused the prices of other assets and investment vehicles to be out of reach for many Americans. The stock market, however, remains accessible for anyone with an internet connection and a little bit of money to invest. Perhaps it’s better for investors to think in terms of how many shares they own vs how many dollars they have.

As always, please consult a financial professional to discuss your unique situation. Click the ‘Contact’ page at the top to schedule an appointment with EVCM and begin your investing journey.

Sources Used:

Why the U.S. Economy and S&P 500 Are Diverging | J.P. Morgan

Why Housing Looks Expensive in Dollars but Cheap in Gold

Priced Out Of 75% Of The Market, Americans' Dream of Homeownership Has Become A Luxury | Bankrate

S&P Cotality Case-Shiller U.S. National Home Price Index (CSUSHPINSA) | FRED | St. Louis Fed