The Three Investors: ROBOs, RIAs and DIYs

The prominence in AI in 2025, and the build-up to it, has companies in many industries re-thinking their business models, and financial services is no different. The rise of the retail investor/trader in the wake of 2020’s pandemic has many questioning the need for money managers and financial advisors in general.

While fiduciary financial advisors, commonly working as a Registered Investment Advisors (RIAs), can provide much more profound services besides just managing your investments, for the purpose of this article we’ll only focus on the returns that these RIAs are typically able to generate for their clients. We’re looking to answer, with unbiased conclusions from data, if a human advisor with discretionary authority over one’s account can provide value in comparison to a ‘robo-advisor’ or a DIY (Do It Yourself) approach.

Some definitions and assumptions:

The Human Advisors we’re focusing on are specifically RIAs that manage retail level investment accounts, typically under $1M USD.

Some examples of ‘Robo-Advisors’ are those from large financial institutions such as SoFi, Fidelity and Vanguard.

The DIY investor is a typical retail investor managing their own self-direct brokerage account.

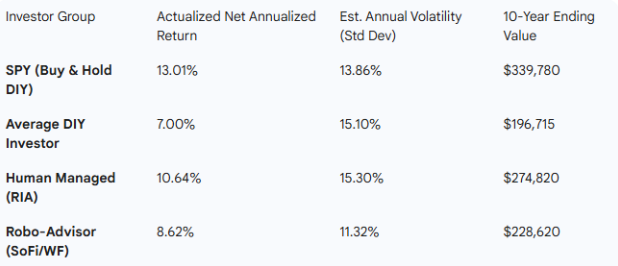

The research compares the annualized returns and volatility of these different investor groups with a $100,000 portfolio generated against the SPY, typically used as the default benchmark for assessing stock market returns, starting January 1, 2016.

The data shows the following:

In summary:

Simply investing in SPY generated the highest returns.

Robo-advisors offered the lowest amount of volatility, indicating that AI or other algorithmic portfolios will focus on diversification for retail investors.

RIAs actually had a similar volatility to DIY retail investors, indicating that even investment professionals can, and do, suffer from biases in their decisions.

DIY retail investors generated the lowest returns, indicating that the average investor can benefit from the use of professional investment management, be it from a human RIA firm or a robo-advisor.

So does this mean all retail investors should simply park their money in SPY and be done? Not necessarily. First, this assumes that an individual investor puts 100% into the SPY and not any individual equities, bonds, options and other financial securities, as well as never sells any portion of their investment. Certainly this isn’t true in most cases and likely never will be.

Additionally, since the data set is only covering the last 10 years (as Robo-advisors and AI began to emerge), there is no prolonged stock market correction, commonly referred to as a ‘Bear Market’, assessed in this timeframe. Indeed there was the shortest bear market in history in 2020 due to the covid crisis and 2022 saw an approximate -18% return in SPY.

With this recency bias in mind, retail investors need to be cognizant of the risks and rewards of investing on their own. Fees will certainly be cheaper investing solely in SPY, but it will require effort to manage one’s portfolio to align on specific goals and avoid catastrophic losses during prolonged downturns.

Each individual investor needs to assess their own needs, goals and investing capabilities to determine if working with a RIA, a Robo-Advisor or using a self-directed brokerage account is right for them.